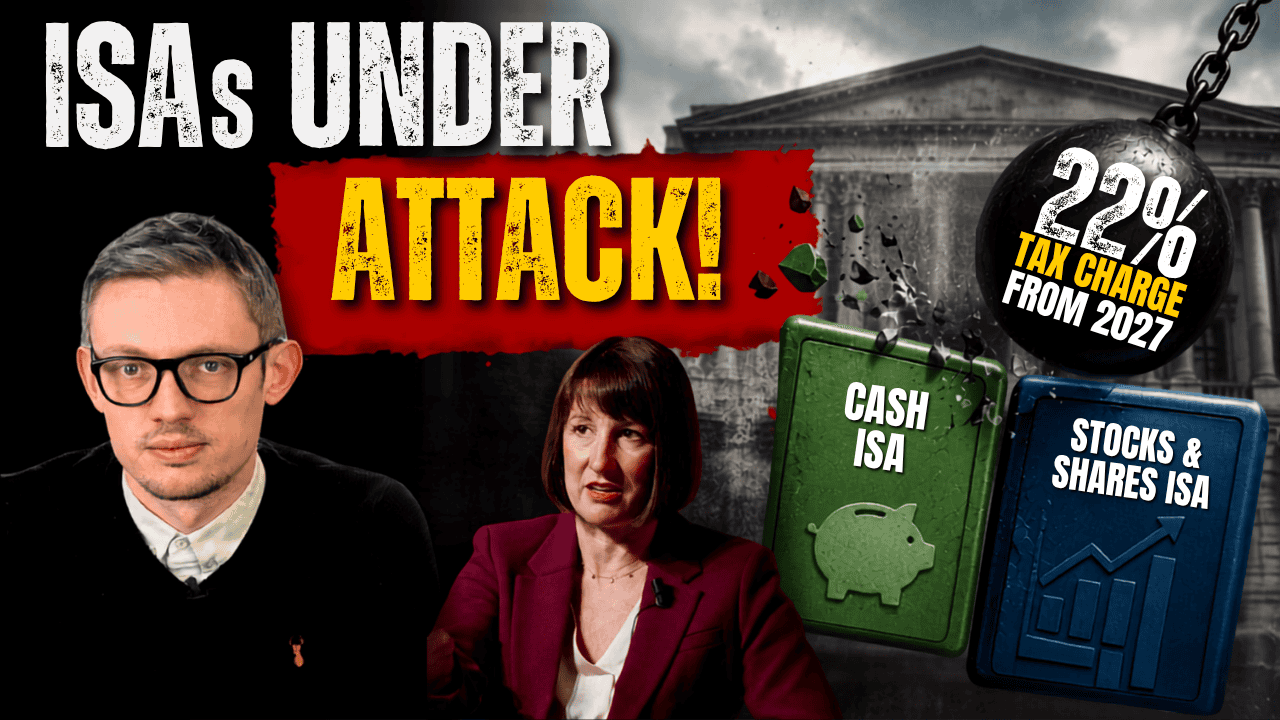

For the first time since their introduction back in 1999, some of the money you hold in an ISA could become subject to tax. In a landmark announcement this week, the Labour Government announced that a flat rate tax charge will start to apply to cash held in a Stocks & Shares ISA from April 2027. This is the second attack on ISAs within 12 months, following the announcement that the Cash ISA allowance will be reduced for under-65s from April 2027. Continue watching as we break down the changes in more detail and assess their impact, but more importantly, look at why ISAs will remain a valuable piece of the Financial Planning puzzle.

Now, before we get into what’s changed, let’s quickly remind ourselves how ISAs work today. Most adults can contribute up to £20,000 each tax year into ISAs. That allowance can be used however you like: you could put the full £20,000 into a Cash ISA, the full £20,000 into a Stocks & Shares ISA, or split it between the two. One of the major benefits of ISAs is that interest, dividends and investment growth are generally free from UK tax. That’s why ISAs remain one of the most valuable planning tools available to us.

However, the Government has already announced that from April 2027, the amount that people under the age of 65 can contribute to Cash ISAs will reduce from £20,000 to £12,000 per year. The overall ISA allowance will remain at £20,000, but if you want to use the full allowance, at least £8,000 would need to go into a Stocks & Shares ISA instead. The Government’s stated aim is to encourage more people to invest for the long term rather than holding large amounts in cash.

We have actually been here before; over a decade ago, the Cash ISA allowance was half of the overall ISA allowance, so this latest initiative from the Government isn’t new, it’s just faded from memory as we enjoyed a 10-year golden age for ISAs.

The concern for the Government is that people might simply add cash into a Stocks & Shares ISA and leave it sitting there uninvested. Alternatively, investors may add £20,000 to a Stocks & Shares ISA and then transfer it all out to a Cash ISA. Technically, this would allow someone to add more than £12,000 in cash whilst still benefiting from the ISA tax wrapper, effectively getting around the new Cash ISA limits.

To prevent this, a new set of anti-circumvention rules has been announced. The headline change is that from April 2027, interest earned on cash held within Stocks & Shares ISAs will be subject to a 22% tax charge; and it’s important to note that this doesn’t just apply to under-65s, it applies to everyone. 22% will be the basic rate tax charge on savings interest from April 2027; currently, 20%. The intention is to remove the tax advantage of holding large amounts of cash inside investment ISAs.

The Government has also announced restrictions designed to prevent people from transferring money from Stocks & Shares ISAs into Cash ISAs in order to bypass the new limits. These new transfer restrictions will only apply to under-65s.

Now, for many investors, this may not make a huge difference. If you’re investing for the long term, cash is often only a temporary holding position while money is being invested or rebalanced. In those situations, the amount of interest generated is likely to be relatively small.

Where it becomes more relevant is for people who deliberately hold larger cash balances inside their investment ISA.

For example, some investors keep one or two years of planned withdrawals in cash. Others hold cash to pay adviser fees or platform charges. Some people have recently sold investments and are waiting for a suitable opportunity to reinvest. These are all perfectly sensible planning strategies, but from April 2027, they may become less tax-efficient than they are today.

However, for those deliberately holding cash to fund short-term planned withdrawals, there may be an alternative that does not run afoul of the new rules. “Money Market funds”, cash-like investments, will be considered eligible to hold within a Stocks & Shares ISA and so will not incur the new tax charges, as long as the whole ISA isn’t made up of 100% Money Market funds.

Finally, there is a small amount of light in the tunnel for high and additional-rate taxpayers. The tax charge of 22% is a flat rate tax charge; it’s not a marginal rate of tax. Ordinarily, with non-ISA cash interest, from April 2027, high-rate taxpayers will be subject to a rate of 42% and additional rate taxpayers will pay 47%. But inside an ISA, the rate will be 22% regardless of your tax status. This means that for higher earners, it still may make sense to deliberately exceed the new £12,000 cash ISA allowance, knowing that although the interest will no longer be tax-free over that amount, it will still be at a more attractive rate than non-ISA savings.

The key message is not that cash becomes bad. Cash still has an important role within a financial plan. Emergency funds, planned spending over the next few years and short-term objectives should often remain in cash because stability can be more important than investment growth. Instead, the planning consideration is simply where that cash is held.

As we move closer to April 2027, investors may need to think more carefully about whether cash should sit inside a Stocks & Shares ISA, inside a Cash ISA, or elsewhere, depending on their circumstances and objectives.

There is also still time before the new regime begins, and the finer details will continue to develop as the Government consults with providers and the industry.

As always, ISA rules are only one piece of the puzzle. The right approach depends on your goals, timescales and wider financial plan. If you’re unsure how these changes might affect you, it’s worth reviewing your arrangements sooner rather than later so there are no surprises when the new rules arrive in 2027.