Another year, another Autumn Budget, but does 2025 bring meaningful change or just more of the same promises? In this, our immediate reaction video, we break down the key announcements, exploring what they could mean for you and your financial planning.

Budget 2025: Buy now, pay later

Yesterday was… eventful. What was already one of the most anticipated Budgets in years turned into what Keir Starmer called “a shambles” after the OBR figures leaked unexpectedly just an hour before the Chancellor stood up. It’s prompted talk of “splashes of mild panic”, even suggestions that the leak might constitute a criminal act. But beyond the drama, this Budget was mild in comparison to the wild speculation that preceded it. Most of the proposed changes are delayed, many of them subtle, and some of them raising real questions about the Government’s long-term strategy.

In this video, we’ll take you through the key announcements, why they matter, and what they could mean for your financial planning.

Before we get into what was announced, let’s have a look at some of the rumours that stayed as just that: rumours. What didn’t happen in the Budget?

One of the biggest pre-Budget fears was a hike in Capital Gains Tax, especially aligning CGT with income tax. This didn’t happen, and rates are untouched.

There was chatter about capping lifetime gifting or abolishing the Inheritance Tax exemption on gifts from surplus income; none of this happened.

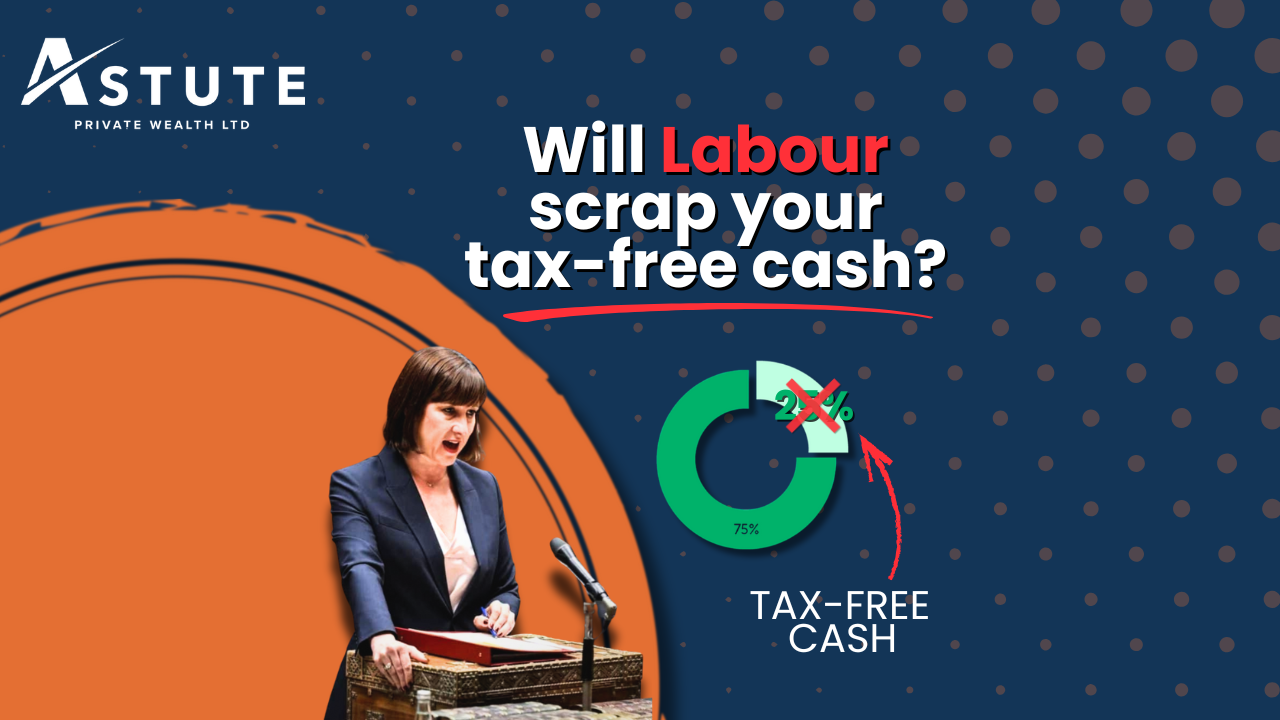

There was speculation that the 25% tax-free pension lump sum might be reduced or capped, as we covered in our video a few weeks ago. Just like the speculation on the same subject in 2024, this came to nought.

Lastly, predictions of reducing higher-rate relief on pension contributions surface every year; still untouched.

Now’s let’s talk about what did happen.

Let’s start with something that wasn’t flashy but is hugely important. Income tax thresholds and allowances, which were already frozen until 2028, will now remain frozen for another three years, until 2031. This is what’s known as a “stealth tax”. The government hasn’t raised rates, so they can technically say they haven’t broken their pledge, but by freezing thresholds, more and more people are dragged into higher tax bands as wages rise. The Chancellor was very deliberate here: big revenue, without technically touching the headline rates.

One of the headline tax rises is the 2% increase across all bands on income from dividends, rental profits and savings interest. For dividends, this kicks in from April 2026, whereas the change to interest and property income is delayed until April 2027. So, if you’re a landlord, an investor relying on dividend income, or someone with large savings outside ISAs, this will bite. For many investors, this reinforces the importance of using tax wrappers efficiently and thinking carefully about how income-producing assets are structured.

Interestingly, this increase will see basic rate taxpayers paying 10% more income tax on rent and interest, whereas higher rate taxpayers will only see a 5% increase.

Another big change: the ISA system is being reformed in April 2027. Under-65s will see their cash ISA allowance reduced to £12,000. You’ll still have the full £20,000 allowance, but the remaining £8,000 will only be available if it’s invested, so stocks and shares, rather than cash. Those aged 65 or over will retain the full £20,000 cash allowance.

This is clearly designed to encourage productive investment, tying in with the Chancellor’s themes of “Invest in Britain”, “Buy, make and sell more here in Britain”, and the promise that “if you build here, Britain will back you.” For cautious savers, though, it does limit how much you can simply hold in cash tax-free.

On the other end of the risk scale, a major change for more adventurous investors came with Venture Capital Trusts. From the next tax year, VCT income tax relief will drop from 30% to 20%. This is a substantial reduction in the upfront benefit, though we don’t see this disincentivising investors from using them.

Lifetime ISAs are being phased out and will be replaced by a new scheme that hasn’t yet been confirmed. This raises big questions for first-time buyers and for younger savers who’ve been relying on the 25% government bonus. We don’t yet know whether that bonus will survive in the new structure, whether existing LISA holders will be protected, or what transitional rules will look like.

A significant long-term change: salary sacrifice arrangements will be capped at £2,000 per year from April 2029. Salary sacrifice has been a widely used way of boosting pension contributions while benefitting from reductions in National Insurance contributions. This cap significantly reduces that planning opportunity and the savings on National Insurance that are available to individuals and employers who engage in salary sacrifice.

It’s unlikely to change behaviours as individuals will still benefit from income tax relief on these pension contributions, but could see their take-home pay reduced by the additional burden of National Insurance. In addition, many employers forward their NI savings to their employees as extra pension contributions, which will now be lost.

From April 2028, properties worth over £2 million will face an additional £2,500 per year in council tax. For properties over £5 million, the surcharge rises to £7,500. This has been speculated about for years, but now we have the confirmation. Politically, it fits with the theme of “a fairer, stronger, more secure Britain”, and targets wealth rather than wages.

Amid all the tax rises, there was one practical announcement: from April 2026, Business Relief and Agricultural Relief allowances of £1mn announced last year will become transferable between spouses. This makes estate planning simpler for many business-owners and farmers, and it brings these reliefs in line with how transferable nil-rate bands work. It also reduces the risk of losing relief when leaving a qualifying asset to a spouse. A sensible change which will be in place when the legislation comes into force in April.

One interesting point is that many of the impactful changes don’t actually kick in for another 18 months, with some, such as the salary sacrifice cap, not being introduced for well over 3 years. That’s raised questions about whether these delayed changes are actually deliverable. But it also allowed the government to avoid immediate pain while still banking revenue in the forecast period, helping them hit that “fiscal firepower” narrative.

Overall, this Budget is less about short-term measures and more about the long-term direction the government wants to set. The numbers yesterday were described as “£22 billion lower than the historic average but double the original number”; another example of the slightly chaotic backdrop to the day.

The key takeaway is that the landscape is shifting. We’re seeing a clear move towards taxing wealth, taxing unearned income, and encouraging productive investment over cash holdings, however there are planning implications across ISAs, pensions, rental income, dividends, and estate planning. As always, if you have any queries about yesterday’s announcements, do not hesitate to contact your Financial Planner.

See you next time.